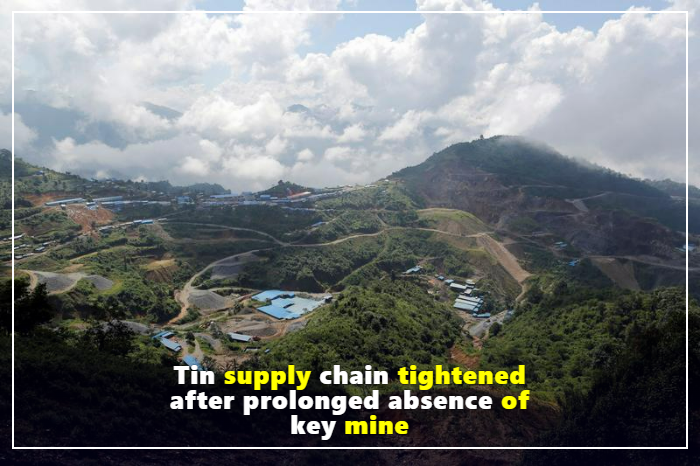

LONDON, Sept 13 (Askume) – It has been more than a year since Myanmar’s Man Maw Tin mine, one of the world’s biggest sources of the strategic metal, stopped production.

While high raw materials and refined tin reserves have so far protected the market from the full impact, this is starting to change.

When authorities of the Wa, an autonomous ethnic group that controls most of Myanmar’s tin resources, ordered a complete suspension of all mining and processing activities in August 2023, most expected the supply shock would last only a few months.

Other small mines in the Wa area have been allowed to reopen. Authorities have also allowed Wenmao to export its above-ground tin stocks, but production remains suspended.

While tin concentrate continues to flow across borders to feed smelters in China, volumes have fallen sharply in recent months, highlighting the lack of activity at the biggest mines.

Dark Maker

The Wa mines are a statistical black hole in global tin supply data. There are no official production statistics and production can only be estimated based on the volume of raw materials passing through Chinese customs.

The International Tin Association estimates Myanmar’s tin output to be around 40,000 tonnes in 2022, with Man Maw accounting for about 70%.

This makes the Wa State the world’s third largest tin producer after China and Indonesia, with Wenmao accounting for 7–8% of global mined supply.

WA officials said the suspension of activities was necessary to audit the tin industry, which has grown rapidly from informal artisanal operations in the early part of the last decade.

In this respect, the Wa State is no different from any other resource-rich country seeking strict property controls.

It’s unclear why the audit took so long.

Reduction in traffic

The impact of the year-long lockdown on China’s import flows is becoming increasingly clear.

In the 10 months after the audit began in August 2023, China imported 100,000 tonnes of Myanmar tin concentrate, compared with 173,000 tonnes in the first 10 months.

Trade between the two countries declined to 11,300 tonnes in the second quarter of this year from 43,600 tonnes in the first quarter, indicating depletion of stocks on land.

Sugar producers have had only limited success in finding alternative sources, with increased imports from Australia, Bolivia and Nigeria not enough to fill the gap.

LSEG data shows that the total import volume of tin raw materials in the first seven months of 2024 fell by 26% compared to the same period last year.

Chinese smelters have begun adjusting maintenance plans and adjusting production plans to compensate.

Yunnan Tin (000960.SZ), the world’s biggest refined tin producer, shut its Yizhou smelter for 45 days in late August.

Provinces such as Yunnan and Jiangxi are cutting production due to feed shortages, according to local data provider Shanghai Metal Market.

fall in stock market

In April 2023, Wa State authorities announced the suspension of tin mining, allowing the Chinese tin industry to accumulate inventory.

Refined tin imports surged in the fourth quarter of 2023, and Shanghai Futures Exchange stocks rose to a record high of 17,818 tonnes in May.

Since then, the registered exchange inventory has been declining and currently stands at 9,499 tonnes. Given that domestic production is being hampered due to the growing shortage of raw materials, the declining trend is likely to continue for at least the next few months.

Since the start of the year, LME tin stocks have fallen by 39% to 4,725 tonnes, although there were still 2,207 tonnes of shadow stocks in LME warehouses as of the end of July.

Western supply chains have been hit harder by a slowdown in Indonesian freight than the Boon Mao incident. Indonesian exports from January to August fell 44% from the same period last year to 24,600 tonnes, due to licensing delays at the start of the year.

risk premium

The tin market was fortunate during the timing of Man Maw’s suspension.

Half of global usage is for circuit board solder, meaning demand is highly sensitive to electronics sales.

Semiconductor sales are a useful indicator of demand for tin solder, but are just emerging from a two-year slump, which helps explain why global tin stocks are so high in the first half of 2024.

Tin still outperforms all other metals traded on the London Metal Exchange by some margin. Three-month tin on the LME was trading at $31,770 a tonne on Friday, up 25% since early January. The second-strongest performer is copper, which is up just 8% year to date.

It is clear that tin prices include a Boon Mao risk premium and will continue to do so until the Wa authorities allow normal operations to resume.

Only the Wa leadership knows the exact time, and they may be focused on other matters.

Although the United Wa State Army is not directly involved in the civil war raging across Myanmar , Bun Mao may not be a priority.

The views expressed in this article are those of the author, a Askume columnist.

The views expressed are solely the author’s own. They do not reflect the views of Askume News, which is committed to integrity, independence and non-partisanship in accordance with the principles of trust.